When Svxy Will Be Over 100 Again

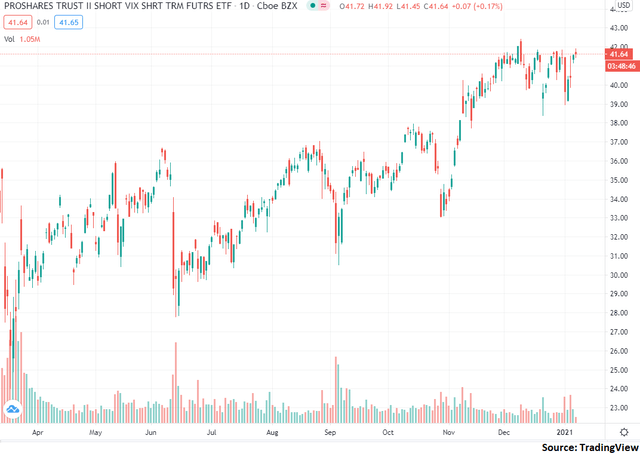

As can be seen in the following nautical chart, the ProShares Short VIX Brusk-Term Futures ETF (BATS:SVXY) has rallied strongly since bottoming in March/April with shares nearing multi-month highs.

Source: TradingView

In my opinion, now is a solid time to buy SVXY if you are long-term investor. I believe the underlying methodology is potent for a long-term play and that investors should consider exposure to this ETF.

Nearly SVXY

To start this piece off, let's talk over the nuances of SVXY's methodology and underlying index. This may seem like a wearisome mode to start off a piece nearly an instrument which purportedly tracks market place volatility, but information technology is essential to grasp the nuance and moving pieces at work in this ETF. Put simply, SVXY is a strong ETF due to its brusk position on an underlying index which has a proven history of destroying wealth.

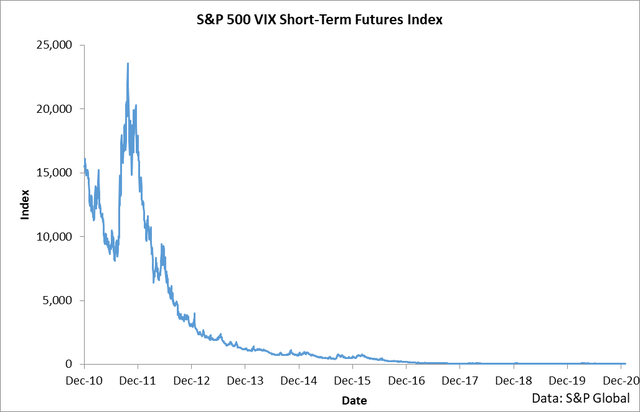

Prior to getting into the fine details, allow's take a mile-loftier await at SVXY. Information technology is an ETF which is shorting something called the S&P 500 VIX Short-Term Futures Alphabetize at half leverage. Why would anyone be interested in shorting this index? Expert question, hither'due south the reply:

Source: Author's calculations of South&P Global data

When I showtime saw the return of this alphabetize, I really idea I was seeing some sort of data error. In fact, in the early on days of VIX-tracking ETPs, I clearly remember opening up my charting platform and skipping a trade in a volatility notation tracking this index due to a belief that I was receiving poor data from my broker.

Unfortunately, for many investors, there is no error in the higher up chart. What you are seeing is an index which has declined in value at an annualized pace of 46% per twelvemonth for the past decade. Yep, information technology has lost about half of its value per twelvemonth for 10 years direct. And this calculation is including the potent volatility rally this year.

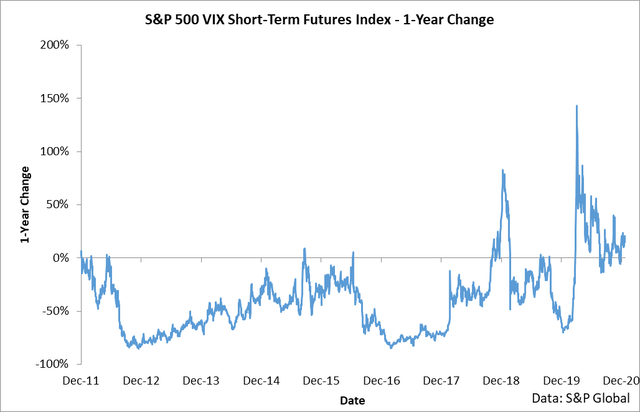

The consistency of losses in this index are really fairly shocking.

Source: Writer's calculations of S&P Global data

On a year-over-year basis, this index has but delivered positive returns to investors for very brief windows. In fact, if you had bought and held this index for one yr at any time during the vii-year period starting in 2011, yous would have had a 97% chance of losing money.

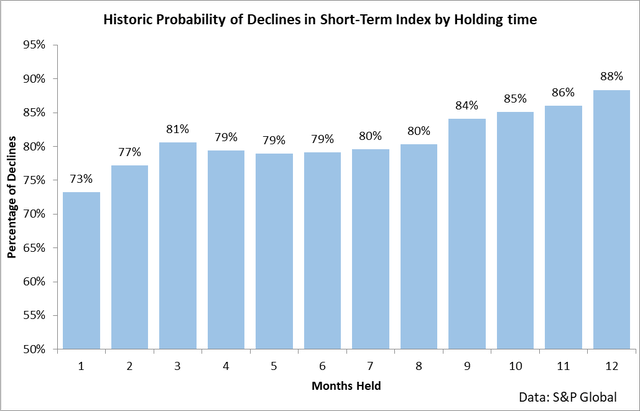

Fifty-fifty over short fourth dimension periods, this index makes for a very poor merchandise.

Source: Author's calculations of South&P Global data

Over the past ten years, the alphabetize has declined in 73% of all months with the probability of losses increasing the longer the holding period. Put simply, this index has not been a favorable investment through time for the vast majority of traders.

And this is where the appeal of SVXY enters the picture. It is an ETF which is shorting this alphabetize at half leverage. An ETF which shorts something that declines almost all of the time should make for a good trade, right? Non then fast. Nosotros've got to talk almost exactly what is driving this relationship prior to trading it and then hash out the risks associated with shorting something linked to the VIX.

The huge problem when it comes to trading VIX futures is this: they tend to exist priced higher than the VIX itself. What I mean by this is that over the past ten years, the front-calendar month VIX futures contract has been higher than the spot level of the VIX in 85% of all trading days.

The reason why this difference in pricing is such a big problem is that futures ultimately converge or reach parity with spot prices. In other words, if you are belongings a futures contract that is priced college than the spot market, as time nears decease, you experience a degree of relative losses every bit your contract slides downwardly towards spot prices.

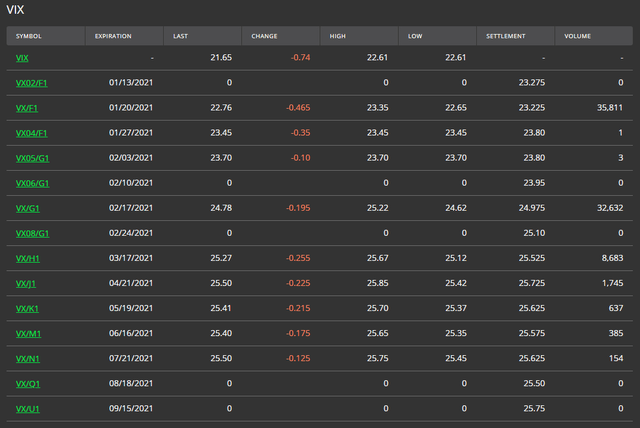

What is so troublesome about VIX futures is the size of the difference between the spot market and VIX contracts. For example, hither is the current VIX market and frontwards curve as provided by CBOE:

Source: CBOE

It may seem like the prices forth the frontwards curve are pretty similar - after all, they are all inside iii-4 points of each other. However, if you get out a calculator, you'll see that the differences in cost are really fairly large.

For example, the February 17th VIX futures contract is currently trading at 24.78 while the VIX is sitting at 21.65. This contract is 14% higher than the spot VIX at the time of writing. Let'southward assume that you were to purchase this futures contract and hold it until decease. Let's too assume that the VIX remains unchanged between now and Feb 17th. If you were to buy this contract and the VIX were to remain unchanged, you would lose 14% on your investment. And that's the trouble.

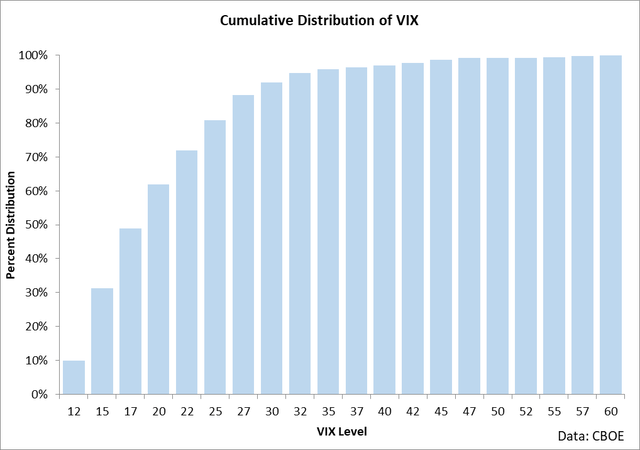

In the long run, the VIX really doesn't get anywhere. What I mean by this is that information technology is almost always betwixt 15 and 25.

Source: Author's calculations of CBOE data

What this ways for VIX futures traders is that futures convergence translates into direct losses to futures holders. Since the VIX doesn't really go anywhere over lengthy periods of time and since futures are almost ever priced above the spot VIX level, futures traders are consistently losing money over the long term as futures curl down and converge with the spot market.

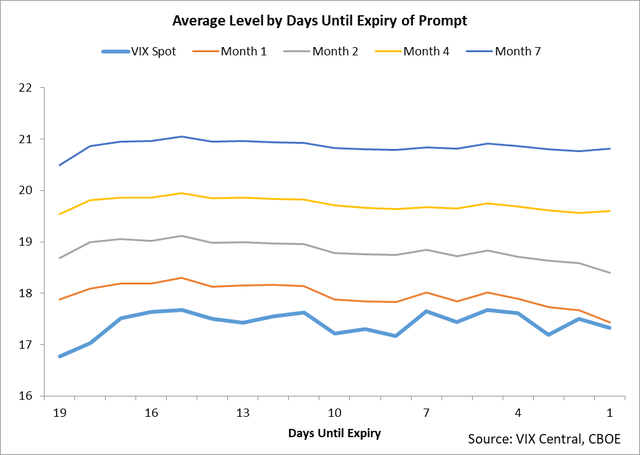

You tin clearly meet this pattern in the data if you group information technology out past days in a trading calendar month.

Source: Author's calculations of VIX Central and CBOE data

In the above chart, I have calculated the boilerplate level of the VIX besides as a few different futures contracts grouped past the days until expiry of whatsoever given month. This chart shows the typical lifecycle of VIX futures contracts during a month. The following relationships are conspicuously seen:

- VIX futures are almost always priced to a higher place the VIX itself

- The greater the time until death, the greater the difference in cost between the spot VIX and futures

- Futures slowly slide downwardly towards spot during the month with the caste of convergence correlated with time until expiry (front end month converges much more strongly than calendar month 2)

The brusk-term futures index (the i SVXY shorts and the one nosotros analyzed above) holds and rolls the front ii contracts. Information technology starts a trading month 100% in the forepart month contract and ends the trading calendar month 100% in the 2nd month contract (at which point the front end contract expires and the 2d contract becomes the forepart contract and everything repeats).

Since this index is holding exposure so closely to the front of the curve, it is exposed to a potent caste of futures convergence which is precisely why it is declining and so strongly through time. And this is exactly why buying SVXY makes for a sound trade.

The key problem though is this: buying SVXY means you're shorting the VIX. And the VIX has been known to brand incredibly stiff movements in very short social club. A stiff movement in the VIX to the upside means a strong movement to the downside in SVXY. For example, SVXY was crushed in the volatility run-up of 2018.

Source: TradingView

The instrument has since reduced leverage to half exposure, but this sort of existential threat remains for those who are simply ownership SVXY on an outright basis.

To alleviate this risk, I would propose either trading it through options or ownership a put to protect the downside. In my opinion, a stop-loss on your position only won't cutting information technology due to gap risk. For a college-hazard approach that lowers the price of trading options, I would suggest ownership the musical instrument outright just also buying a put option deeply out of the money.

Regardless, the point I want to stress here is this: yes, SVXY is a good purchase, and yes, it is likely going to continue pushing college, but firm risk management hedges must be in identify to trade this instrument in my stance. All this said, SVXY is likely headed higher due to the clear futures convergence issues present in VIX futures.

Decision

SVXY is an instrument which is built effectually shorting an index that declines about all of the time. The primary reason to purchase SVXY over lengthy fourth dimension periods is its ability to capture futures convergence. If y'all are going merchandise SVXY, hedge the position using options.

This article was written by

I work inside the trading and money management manufacture. I have been trading and investing for several years. My style is technical execution with a fundamental thesis in place. I rely heavily on statistical assay of the correlations between fundamental changes and toll movements for generating near ideas.

Disclosure: I am/we are short UVXY. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business human relationship with any company whose stock is mentioned in this article.

Source: https://seekingalpha.com/article/4397979-svxy-solid-long-term-volatility-play

{kind=link}

Postar um comentário for "When Svxy Will Be Over 100 Again"